Summary: Rental income is taxable - but the IRS and Oregon allow landlords to deduct a wide range of operating expenses that can significantly reduce what you actually owe. This guide walks through every major deduction category available to Portland landlords in 2026, including some lesser-known ones, and explains how Oregon's state and local tax obligations layer on top of federal rules.

⏱ 6-minute read

What Expenses Can I Deduct as a Portland Landlord?

One of the most financially meaningful things you can do as a rental property owner is understand your tax deductions - and actually use them. The IRS taxes landlords on net rental income, not gross rent collected. That distinction matters enormously. Used correctly, deductions can reduce your taxable income to a fraction of what your rent roll shows.

At Uptown Properties, we work with Portland landlords every day, and tax efficiency is one of the areas where we consistently see money left on the table - not through anything complicated, but simply because landlords aren't aware of everything they're entitled to deduct.

Here's a thorough, Portland-specific breakdown. Note: this article is educational and not a substitute for advice from a qualified CPA or tax professional. Oregon's tax rules have specific nuances, and a professional familiar with investment real estate will help you apply these correctly to your situation.

The Foundation: How Rental Income Is Taxed

Rental income is reported on Schedule E of your federal Form 1040, per IRS guidelines. This is where you report both your gross rental income and your deductible expenses, arriving at a net figure that flows to your overall tax return.

Oregon follows federal treatment closely for most rental income purposes. State income tax in Oregon ranges from 4.75% to 9.9% depending on your income bracket, and rental income is included in that calculation. You'll report Oregon rental income on Form OR-40 if you're a full-year resident.

If you expect to owe $1,000 or more in federal taxes after withholding and credits, the IRS requires quarterly estimated tax payments using Form 1040-ES. Oregon similarly requires estimated payments using Form OR-40-V. Missing these can result in underpayment penalties even if you pay in full at filing.

The Big Ones: Deductions That Move the Needle Most

Depreciation

Depreciation is often the single largest deduction available to rental property owners, and it's one many landlords underutilize. The IRS allows you to recover the cost of a residential rental building - not the land - over 27.5 years using the Modified Accelerated Cost Recovery System (MACRS).

Here's how the math works: if you purchased a property for $400,000 and the land is valued at $80,000, your depreciable basis is $320,000. Divide that by 27.5 and you get approximately $11,636 per year in depreciation you can deduct - without spending a dime. That's a non-cash deduction that reduces your taxable income every single year you own the property.

One critical point: the IRS requires you to recapture depreciation when you sell, whether or not you claimed it. Skipping depreciation doesn't help you avoid recapture - it just means you gave up the deduction for no benefit. Always claim it.

Under the One Big Beautiful Bill Act signed in 2025, 100% bonus depreciation has been permanently restored at the federal level for qualifying property. This means certain improvements and personal property components - appliances, flooring, fixtures - may be fully deductible in the year they're placed in service rather than depreciated over time. Oregon uses Schedule OR-DEPR for state depreciation tracking, which may differ from your federal treatment in some cases - another reason to work with a CPA familiar with Oregon investment property.

Mortgage Interest

Interest paid on your rental property mortgage is fully deductible as a business expense on Schedule E, up to $750,000 in loan value for single and joint filers. Your lender will provide IRS Form 1098 each year showing your total mortgage interest paid. If you used a HELOC to fund property improvements, that interest may also qualify.

Property Taxes

Property taxes paid on investment property are fully deductible on Schedule E - and unlike the SALT cap that applies to homeowners, there is no cap on this deduction for rental property owners. Portland's property tax rate is approximately 2.6% of assessed value, due as a lump sum on November 15 or in installments on November 15, February 15, and May 15. Every dollar you pay is a deductible expense.

Oregon's Measure 50 caps annual increases in assessed property value at 3% unless there are improvements or ownership changes, which provides some predictability in this expense line.

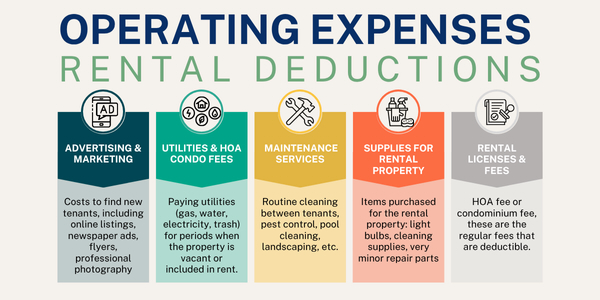

Operating Expenses: What You Can Deduct in Full

The IRS allows landlords to deduct ordinary and necessary expenses incurred in managing, conserving, and maintaining a rental property. The following are fully deductible in the year they're paid:

Insurance premiums: Landlord insurance, liability coverage, and any supplemental policies for your rental property are deductible operating expenses.

Property management fees: If you work with a property management company, their fees are fully deductible. For most Portland landlords, this runs 8–10% of gross rents collected.

Repairs and maintenance: Costs to keep the property in good working condition are immediately deductible. This includes fixing plumbing issues, patching drywall, replacing a broken appliance, repainting, and routine maintenance. The key distinction is that repairs restore something to its original condition - they don't improve or add value beyond what existed before.

Advertising and leasing costs: Listing fees, photography, tenant screening costs, and any marketing expenses to find tenants are deductible.

Professional and legal fees: Attorney fees related to lease drafting, eviction proceedings, or lease disputes are deductible, as are accounting and tax preparation fees specific to your rental activity.

Utilities paid by the landlord: If you pay water, sewer, garbage, or any other utility for the property, those costs are deductible.

Travel and mileage: Trips to your rental property for repairs, inspections, or tenant issues are deductible. The IRS standard mileage rate for business use applies. Keep a mileage log.

HOA Fees

If your rental property is subject to a homeowners association, your regular HOA dues are fully deductible as an ordinary operating expense on Schedule E - no different than insurance or property management fees. Because the property is a rental rather than a primary residence, there is no limitation on this deduction.

One nuance to be aware of: if the HOA levies a special assessment for a capital improvement - a new roof on a shared building, for example, or a parking structure upgrade - that cost may need to be capitalized and depreciated rather than expensed in full in the year it's paid. The same repair vs. improvement logic covered above applies. Routine monthly or annual dues have no such issue and are simply deductible in the year paid.

Repairs vs. Improvements: A Distinction That Matters

This is one of the most common areas where landlords make costly mistakes. The IRS draws a clear line between repairs and improvements, and misclassifying them can trigger audit issues.

A repair restores something to its prior condition and is immediately deductible. Patching a roof leak, replacing a broken garbage disposal, or fixing a damaged floor are repairs.

An improvement adds value, extends the property's useful life, or adapts it to a new use - and must be capitalized and depreciated over time, typically over 27.5 years. A full roof replacement, a kitchen remodel, adding a deck, or installing a new HVAC system are improvements.

The IRS applies what's called the "betterment, restoration, or adaptation" test under the tangible property regulations. One useful exception: the De Minimis Safe Harbor rule allows you to fully expense any single item costing $2,500 or less per invoice without capitalizing it. Document everything with receipts and photos.

Portland and Multnomah County: Local Taxes to Know

Portland landlords have additional local tax obligations that don't apply everywhere in Oregon.

Portland and Multnomah County Business Tax - Portland collects a business tax of 2.6% and Multnomah County collects 2% on the net proceeds of rental business activity conducted within the city or county. If your rental property is in Portland, this applies to you and the fees are themselves deductible as a business expense.

Residential Rental Registration - Portland requires landlords to register rental units and pay an annual fee. This registration cost is a deductible operating expense.

Both of these are easy to overlook but important to stay current on - both for compliance and because they're legitimate deductions.

A Few Deductions Landlords Often Miss

Home office deduction - If you have a dedicated space in your home used exclusively for managing your rental business, it may qualify as a deductible home office expense. It must be used regularly and exclusively for rental management activity.

Education and professional development - Books, courses, or seminars related to property management or real estate investing may qualify as deductible business education expenses.

Passive loss rules - If your rental property shows a loss on Schedule E, you may be able to deduct up to $25,000 of that loss against ordinary income if you actively participate in managing the property and your modified adjusted gross income is $100,000 or below. The deduction phases out between $100,000 and $150,000. Above $150,000, passive loss rules generally prevent using rental losses to offset ordinary income unless you qualify as a real estate professional under IRS guidelines.

Keep Records All Year, Not Just at Tax Time

The IRS expects documentation for every deduction you claim. That means receipts, invoices, bank statements, mileage logs, and records of repairs with dates and descriptions. The repair-vs.-improvement distinction is a frequent audit trigger, and good documentation is your best defense.

A simple system - even a folder of receipts organized by category - goes a long way. Many landlords use property management software or accounting tools to track income and expenses automatically throughout the year.

We Can Help

Managing the financial side of a rental portfolio is one of the most time-consuming parts of being a landlord. At Uptown Properties, our property management services include organized financial reporting that makes tax season significantly less stressful - and ensures the documentation your CPA needs is already in order.

Whether you're looking for help managing your property, thinking about adding to your portfolio, or just getting started as a Portland landlord, our team is here.

- Own a rental property? We manage Portland properties with full financial reporting and owner transparency.

- Thinking about buying? Our brokerage team can help you evaluate investment properties with the full tax picture in mind.

- Looking for a rental? We manage quality homes across the Portland metro.